The U.S. Debt Problem, Explained: China’s Treasury Signal & The Price of America’s Deficits

In a report by Bloomberg a few days ago, China has reportedly asked state-linked banks to reduce their exposure to U.S. Treasuries.

Not liquidate. Not weaponise. Reduce.

At first glance, that might seem incremental. China’s holdings of U.S. government debt peaked more than a decade ago, above $1.3 trillion around 2013. The latest U.S. Treasury TIC data place that figure materially lower, closer to the $750–800 billion range. The direction has been steady.

But timing matters.

The United States is running a federal deficit north of $1.5 trillion annually. In fiscal year 2023, the deficit came in around $1.7 trillion. Gross federal debt has crossed $34 trillion and continues to climb. Net interest outlays are now one of the fastest-growing line items in the federal budget, approaching $880–900 billion a year, and projected by the Congressional Budget Office to exceed $1 trillion annually within the next few years.

When your borrowing costs are already climbing, even marginal shifts in demand start to matter.

You see, this isn’t about China exiting the dollar system.

It’s about what happens when the buyer base for U.S. debt becomes less automatic.

The Architecture of Cheap American Debt

The United States has long benefited from an unusual asymmetry.

Foreign investors hold roughly $68-69 trillion worth of U.S. assets - spanning Treasuries, corporate bonds, equities, real estate and direct investment. Meanwhile, U.S. investors hold about $40-41 trillion in foreign assets.

That leaves a gap of nearly $28 trillion. That is just shy of the U.S. GDP.

Put differently: the rest of the world is structurally long on America.

This imbalance is reflected in the U.S. net international investment position (NIIP), which has been negative by roughly $18–20 trillion in recent readings. In most countries, a negative NIIP of that magnitude would be destabilising.

In the U.S., it has been fundable.

Why? Because the dollar remains the primary reserve currency. Roughly 58-60% of global allocated foreign exchange reserves are held in dollars, according to IMF COFER data. The euro accounts for about 20%. The yen and sterling sit in single digits.

The U.S. Treasury market itself is enormous - about $25 trillion outstanding. No other sovereign market approaches that depth. German Bunds are a fraction of that size. Japanese government bonds are large but less globally central as collateral and settlement instruments.

This is the plumbing of reserve privilege.

Surplus economies earn dollars through trade. Those dollars are recycled into U.S. Treasuries, agency bonds, corporate debt and equities. In 2022–23, foreigners held roughly a quarter to a third of the Treasury market - around $7–8 trillion.

More demand means lower yields.

Lower yields mean cheaper funding for Washington.

That relationship has underwritten decades of deficit tolerance.

The Refinancing Wall

Now layer in arithmetic.

The U.S. Treasury will refinance trillions of dollars of maturing debt over the next few years while continuing to issue new debt to cover deficits. In some projections, more than $7-8 trillion worth of securities mature in 2026 alone.

Average interest rates on newly issued debt have risen sharply compared to the ultra-low-rate era of 2010–2021. In 2020, the weighted average interest rate on federal debt hovered near historic lows, around 1.5–2%. Today, new issuance across maturities often clears closer to 4–5%, depending on tenor.

But you see, that difference compounds, very fast.

According to data from U.S. Debt Clock, the latest numbers look something like this:

Net interest payments: ~$988 billion

Defence spending: ~$929 billion

Interest payments has overtaken the U.S. military spending as of writing this article, in 2026 and is on track to overtake major spending categories like social security and U.S. Medicare in the probably not-too-distant future.

To help you understand the sensitivity: a 100-basis point (1 percentage point) increase in average borrowing costs applied to tens of trillions of debt eventually translates into hundreds of billions of dollars in additional annual interest over time.

If yields drift from around 4.1% toward 5.1% on the long end, the federal budget arithmetic changes materially.

That is why demand elasticity matters.

You get why the U.S. is worried. You now know why there is a tussle between President Trump and the sitting U.S. Federal Reserve chairman, Jerome Powell. Trump wants Powell to reduce interest rates, to pay less in payments to global lenders, at the cost of depreciating the U.S dollar, but the Fed chairman is unwilling to do so, fearing a further spike in inflation in America, triggered by this flood of freshly printed money.

The Long Drift in Foreign Demand

China’s Treasury holdings have declined from above $1.3 trillion in 2013 to below $800 billion recently. Its share of total foreign-held Treasuries has fallen meaningfully.

Japan remains the largest individual foreign holder, with holdings still around or above $1 trillion. The U.K. has emerged as a large holder, often exceeding $600-700 billion. Belgium and Luxembourg frequently appear high in the rankings - partly due to custodial accounts and clearing structures.

Total foreign holdings of Treasuries have not collapsed. They remain substantial. But growth has been uneven.

Meanwhile, central banks have been buying gold at record pace. According to the World Gold Council, official sector gold purchases exceeded 1,000 tonnes in both 2022 and 2023 - among the highest annual totals on record. China has reported adding to its gold reserves consistently. India’s gold reserves have risen steadily over the past several years.

At the same time, the share of U.S. Treasuries in global reserve portfolios has edged lower compared to the early 2000s, even as the dollar’s overall reserve share remains dominant.

No dramatic exit.

But incremental diversification.

And incremental changes shift marginal demand.

The Dollar and Relative Currency Moves

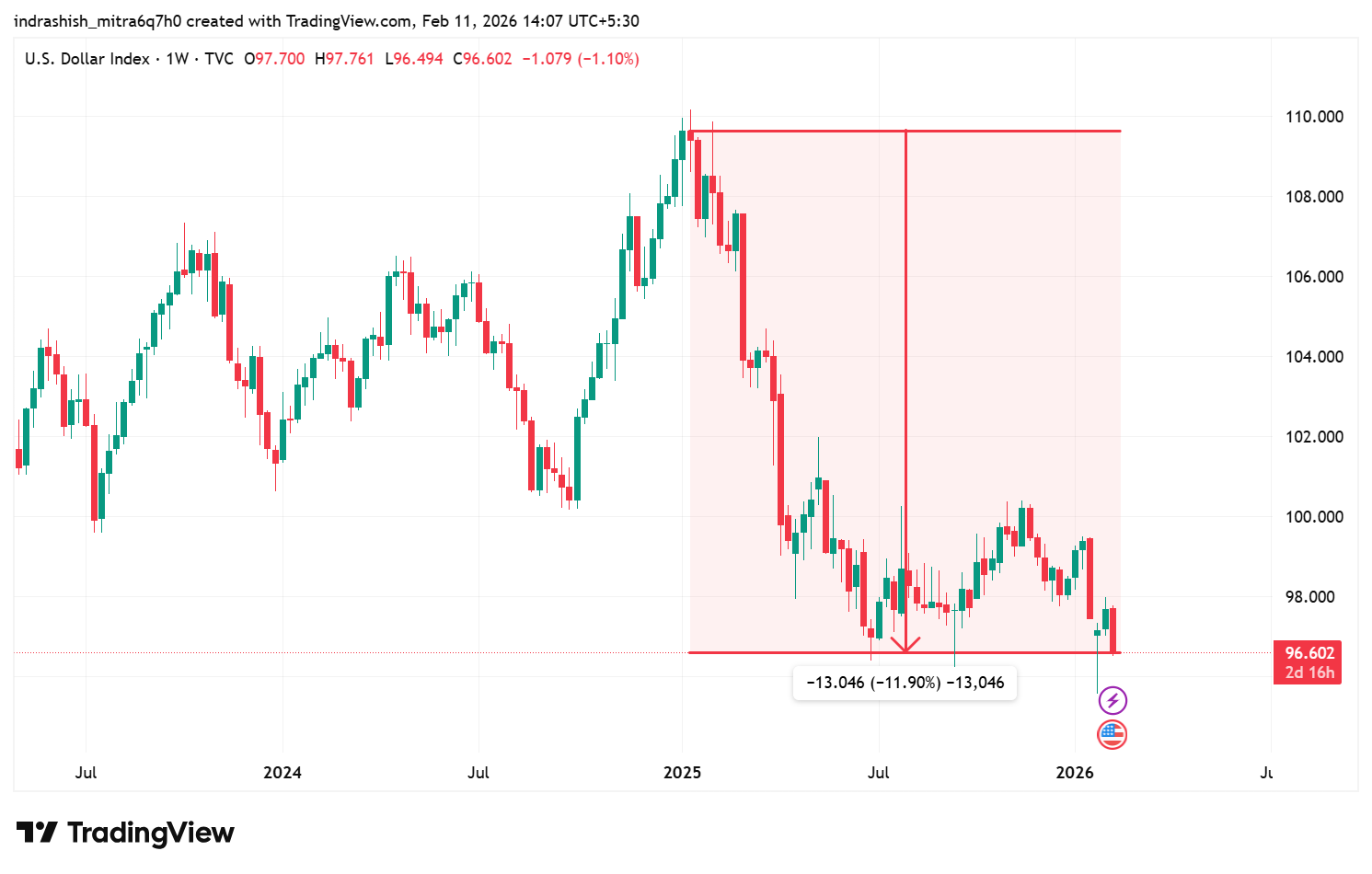

The U.S. Dollar Index (DXY) surged in 2022, touching multi-decade highs above 110 during peak tightening and energy stress. Since then, it has moderated, fluctuating closer to the 100-105 range in subsequent periods. More notably, since the beginning of 2025, the dollar index has been down just shy of 12%.

It remains strong by historical standards. But the momentum is no longer one-directional.

Meanwhile:

The Japanese yen, which weakened beyond 150 per dollar at points, has seen episodes of recovery as expectations around Bank of Japan policy normalisation have increased.

The Chinese yuan, while managed within a controlled band, has avoided sharp destabilisation and remains central to regional trade settlement expansion.

The Indian rupee has traded in a relatively stable corridor, supported by foreign capital inflows into equities and bonds and active RBI management.

These are not dramatic shifts.

But they illustrate that the dollar’s dominance does not preclude relative currency resilience elsewhere.

If fewer countries are expanding Treasury holdings aggressively, currency dynamics gradually reflect that recalibration.

The Marginal Buyer Problem

Now here’s where the mechanics sharpen.

Treasury auctions depend on a mix of:

Primary dealers

Foreign official institutions

Domestic pension funds

Insurance companies

Asset managers

When demand is robust, the government can issue large volumes of debt with minimal yield disruption. When demand growth slows, yields must rise to entice incremental buyers.

Recent data show that the term premium - measured by the New York Fed’s ACM model - has moved higher compared to the deeply negative levels seen during quantitative easing. The 30-year yield has, at times, risen more sharply than the 5-year yield, reflecting increased compensation for long-duration risk.

This is not crisis behaviour. Bid-to-cover ratios remain within historical norms.

But sensitivity has increased.

If foreign official buyers - historically price-insensitive - reduce participation, private investors must absorb more supply. Private investors demand yield compensation.

And when supply is rising, even small reductions in foreign participation can push yields upward at the margin.

Europe’s Position

Europe collectively remains deeply invested in U.S. financial markets - across Treasuries, corporate bonds and equities. Transatlantic financial exposure runs into trillions of dollars.

At the same time, political rhetoric around tariffs, industrial subsidies and strategic autonomy has intensified. European leaders have publicly discussed preparedness to respond to trade escalation. Opinion surveys suggest public perceptions of the U.S. in Europe have cooled relative to past decades.

There is no evidence of coordinated Treasury retaliation.

But capital discussions have entered political language. From Davos to bilateral conversations.

Once that happens, permanence becomes conditional.

Markets price conditionality.

Understanding The Cost Cascade

Higher Treasury yields do not remain contained in Washington.

If long-term yields rise:

30-year mortgage rates rise.

Corporate bond spreads adjust.

Small business financing costs increase.

Consumer credit becomes more expensive.

The U.S. government itself pays more to service its obligations.

With gross debt above $34 trillion, the scale is unforgiving. Even if only a portion refinances each year, the weighted average cost drifts higher over time.

And as interest payments rise, deficits can widen further unless offset by spending cuts or revenue increases.

That feedback loop is structural.

Russia-Ukraine War: The Precedent Effect

The freezing of roughly €300 billion in Russian reserves in 2022 introduced a new dimension into sovereign asset allocation. Assets once considered politically neutral became instruments of enforcement.

For reserve managers globally, that precedent is not ignored.

It does not trigger immediate liquidation.

But it encourages diversification into assets that sit outside another sovereign’s balance sheet - including gold.

That diversification trend aligns with the data.

What This Was - And Wasn’t

It’s important to draw a clean line here.

Because when trends like this emerge, it’s easy to leap from direction to destiny.

That’s not what this is.

What we are observing is an accumulation of signals - data points, policy nudges, shifts in allocation patterns. Interpreted together, they suggest a change in tone. They do not confirm an outcome.

So let’s be precise.

It was:

A reported Chinese directive asking state-linked banks to reduce exposure to U.S. Treasuries.

A continuation of a diversification trend that has been underway since China’s Treasury holdings peaked more than a decade ago.

A reminder that persistent U.S. fiscal deficits are sustained, in part, by foreign capital participation.

A moment in which refinancing needs are elevated and interest costs are already rising.

These are facts. Observable. Measurable.

It wasn’t:

A coordinated liquidation of U.S. debt.

A formal policy announcement of financial confrontation.

Evidence of imminent dollar collapse.

A breakdown in Treasury market functioning.

Treasury auctions are still clearing.

Foreign holdings remain substantial.

The dollar continues to anchor global trade and reserves.

You see, the future being implied in some corners - de-dollarisation, funding stress, systemic rupture. But it is not confirmed. It is not forecast here. It is not inevitable.

There are innumerable number of factors at play here.

What we are examining is the interaction of arithmetic and behaviour.

When foreign demand becomes more selective, borrowing costs can drift higher.

When borrowing costs drift higher, interest expenses rise.

That is mechanism, not prophecy.

The Treasury market remains the deepest in the world. The dollar remains dominant. The U.S. remains central to global finance.

But dominance is not immunity from arithmetic.

The Structural Recalibration

For decades, global capital flowed into U.S. assets almost reflexively. Surplus countries recycled earnings. Central banks accumulated Treasuries. Yields remained anchored even as debt rose.

Now, flows appear more selective.

Not reversed. Selective.

If China trims exposure from $1 trillion-plus levels to below $800 billion, if Europe recalibrates purchases, if Japan’s domestic yields rise, if central banks continue accumulating gold - the cumulative effect is gradual repricing.

When funding is automatic, deficits feel manageable.

When funding requires persuasion, yields adjust.

The United States can still finance itself at scale. It retains unmatched liquidity, legal infrastructure and enforcement power.

But its interest bill is already approaching $900 billion annually - on track to cross $1 trillion. Its debt-to-GDP ratio has crossed 124%.

In that context, the difference between abundant foreign demand and cautious foreign demand is measured not in headlines, but in basis points.

And basis points, when applied to trillions, become policy constraints.

China’s move may not change the system.

But it highlights something fundamental: America’s cheap debt has always depended on global participation.

If that participation becomes conditional - even marginally - the cost of capital edges higher.

Not collapse. Recalibration.

And in sovereign bond markets, recalibration is rarely dramatic. It shows up first in spreads, in term premiums, in interest line items buried deep inside a federal budget.

That is where this story is unfolding.

Disclaimer:

This article is for informational and educational purposes only. It does not constitute financial, investment, or trading advice and should not be relied upon as such. There is no guarantee of any investment gains, and readers are encouraged to conduct their own research before making any investment decisions.